Note

Go to the end to download the full example code

Example: Stochastic Volatility¶

Generative model:

\begin{align}

\sigma & \sim \text{Exponential}(50) \\

\nu & \sim \text{Exponential}(.1) \\

s_i & \sim \text{Normal}(s_{i-1}, \sigma^{- 2}) \\

r_i & \sim \text{StudentT}(\nu, 0, \exp(s_i))

\end{align}

This example is from PyMC3 [1], which itself is adapted from the original experiment from [2]. A discussion about translating this in Pyro appears in [3].

We take this example to illustrate how to use the functional interface hmc. However, we recommend readers to use MCMC class as in other examples because it is more stable and has more features supported.

References:

Stochastic Volatility Model, https://docs.pymc.io/notebooks/stochastic_volatility.html

The No-U-Turn Sampler: Adaptively Setting Path Lengths in Hamiltonian Monte Carlo, https://arxiv.org/pdf/1111.4246.pdf

Pyro forum discussion, https://forum.pyro.ai/t/problems-transforming-a-pymc3-model-to-pyro-mcmc/208/14

import argparse

import os

import matplotlib

import matplotlib.dates as mdates

import matplotlib.pyplot as plt

import jax.numpy as jnp

import jax.random as random

import numpyro

import numpyro.distributions as dist

from numpyro.examples.datasets import SP500, load_dataset

from numpyro.infer.hmc import hmc

from numpyro.infer.util import initialize_model

from numpyro.util import fori_collect

matplotlib.use("Agg") # noqa: E402

def model(returns):

step_size = numpyro.sample("sigma", dist.Exponential(50.0))

s = numpyro.sample(

"s", dist.GaussianRandomWalk(scale=step_size, num_steps=jnp.shape(returns)[0])

)

nu = numpyro.sample("nu", dist.Exponential(0.1))

return numpyro.sample(

"r", dist.StudentT(df=nu, loc=0.0, scale=jnp.exp(s)), obs=returns

)

def print_results(posterior, dates):

def _print_row(values, row_name=""):

quantiles = jnp.array([0.2, 0.4, 0.5, 0.6, 0.8])

row_name_fmt = "{:>8}"

header_format = row_name_fmt + "{:>12}" * 5

row_format = row_name_fmt + "{:>12.3f}" * 5

columns = ["(p{})".format(int(q * 100)) for q in quantiles]

q_values = jnp.quantile(values, quantiles, axis=0)

print(header_format.format("", *columns))

print(row_format.format(row_name, *q_values))

print("\n")

print("=" * 20, "sigma", "=" * 20)

_print_row(posterior["sigma"])

print("=" * 20, "nu", "=" * 20)

_print_row(posterior["nu"])

print("=" * 20, "volatility", "=" * 20)

for i in range(0, len(dates), 180):

_print_row(jnp.exp(posterior["s"][:, i]), dates[i])

def main(args):

_, fetch = load_dataset(SP500, shuffle=False)

dates, returns = fetch()

init_rng_key, sample_rng_key = random.split(random.PRNGKey(args.rng_seed))

model_info = initialize_model(init_rng_key, model, model_args=(returns,))

init_kernel, sample_kernel = hmc(model_info.potential_fn, algo="NUTS")

hmc_state = init_kernel(

model_info.param_info, args.num_warmup, rng_key=sample_rng_key

)

hmc_states = fori_collect(

args.num_warmup,

args.num_warmup + args.num_samples,

sample_kernel,

hmc_state,

transform=lambda hmc_state: model_info.postprocess_fn(hmc_state.z),

progbar=False if "NUMPYRO_SPHINXBUILD" in os.environ else True,

)

print_results(hmc_states, dates)

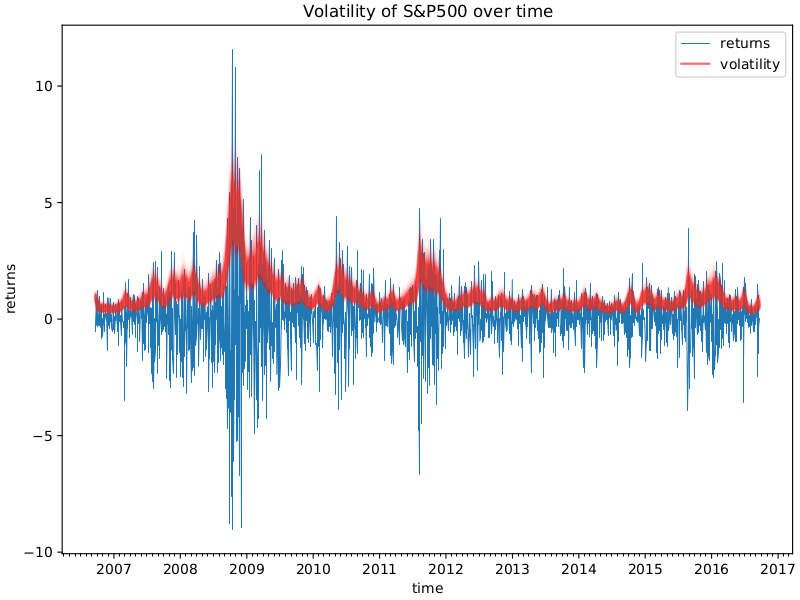

fig, ax = plt.subplots(figsize=(8, 6), constrained_layout=True)

dates = mdates.num2date(mdates.datestr2num(dates))

ax.plot(dates, returns, lw=0.5)

# format the ticks

ax.xaxis.set_major_locator(mdates.YearLocator())

ax.xaxis.set_major_formatter(mdates.DateFormatter("%Y"))

ax.xaxis.set_minor_locator(mdates.MonthLocator())

ax.plot(dates, jnp.exp(hmc_states["s"].T), "r", alpha=0.01)

legend = ax.legend(["returns", "volatility"], loc="upper right")

legend.legendHandles[1].set_alpha(0.6)

ax.set(xlabel="time", ylabel="returns", title="Volatility of S&P500 over time")

plt.savefig("stochastic_volatility_plot.pdf")

if __name__ == "__main__":

assert numpyro.__version__.startswith("0.14.0")

parser = argparse.ArgumentParser(description="Stochastic Volatility Model")

parser.add_argument("-n", "--num-samples", nargs="?", default=600, type=int)

parser.add_argument("--num-warmup", nargs="?", default=600, type=int)

parser.add_argument("--device", default="cpu", type=str, help='use "cpu" or "gpu".')

parser.add_argument(

"--rng_seed", default=21, type=int, help="random number generator seed"

)

args = parser.parse_args()

numpyro.set_platform(args.device)

main(args)